Use this calculator to determine the home equity line of credit amount you may qualify to receive. The line of credit is based on a percentage of the value of your home, which is also known as loan-to-value (LTV). The more your home is worth, the larger the line of credit. Of course, the final line of credit you receive will take into account any outstanding mortgages you might have. This includes first mortgages, second mortgages and any other debt you have secured by your home.

For your convenience we publish current El Monte HELOC & home equity loan rates and El Monte mortgage rates below.

The following table shows current El Monte 30-year mortgage rates. You can use the menus to select other loan durations, alter the loan amount, change your down payment, or change your location. More features are available in the advanced drop down.

Our rate table lists current home equity offers in your area, which you can use to find a local lender or compare against other loan options. From the [loan type] select box you can choose between HELOCs and home equity loans of a 5, 10, 15, 20 or 30 year duration.

One benefit of home ownership is the ability to use earned equity to borrow the money you need. There are different ways that people might harness the value of the equity, depending on their own goals, situation and opportunities.

There are really three options that most people will look to when seeking to use their equity:

Cash-out Refinance

A cash-out refinance, is really a refinancing of your existing mortgage with an additional lump sum added in, to be spent as you see fit. This can be viewed most simply as one loan replacing another.

Home Equity Loan

A home equity loan, is a lump sum payment as well, but it does not include your mortgage payment – it is in addition to your mortgage, so is sometimes referred to as a second mortgage. The first mortgage has a senior position in the capital structure, but if you default on either loan you could still lose the house.

Home Equity Line of Credit

A HELOC is similar to a home equity loan in terms of working alongside your existing first mortgage, but it acts more like a credit card, with a draw period, and a repayment period and is one of the more popular options with today’s homeowners.

Each option can be strategic, depending on your own circumstances – so understanding more about why you’d choose one over the other can help you to focus your research.

| Loan Type | Home Equity Loans | HELOC | Cash Out Refi |

|---|---|---|---|

| Interest Rate | Fixed | Adjustable (in most cases) | Fixed |

| Draw Money | Lump Sum | As needed, throughout draw period | Lump Sum |

| Tax Deductible Interest | No | No | Yes |

| Interest Only Payment | No | Yes | No |

| Interest On | Loan Amount | Amount Drawn | Loan Amount |

As the Federal Reserve has lifted short-term interest rates in the late 2010s many homeowners who typically opted for the cash-out refi option in the prior decade became more inclined to use a home equity loan or line, so they keep their existing low rate on the majority of their home debt. Then as the COVID-19 crisis struck interest rates crashed to the floor, shifting homeowner preference back toward cash out refinancing.

This article will look at some of the details and specifics of HELOCs in an effort to allow you to make a better choice when you are comparing options. You should refer to the guidance of a trusted financial advisor before making any major financial move.

After the Great Recession many United States homeowners were in negative equity, with 26% of mortgaged properties having negative equity in the third quarter of 2009. As of the end of the second quarter of 2018 only 2.2 million homes, or 4.3% of mortgaged properties remained in negative equity. CoreLogic estimated that in the second quarter of 2018 U.S. homeowners saw an average increase of equity of $16,200 for the past 12 months, while key states like California increased by as much as $48,000.

Over the past 12 months homeowners saw an average equity increase of 12.3%, for a total increase of $980.9 billion. This means the 63% of homes across the United States with active mortgages now have around $8.956 trillion in equity.

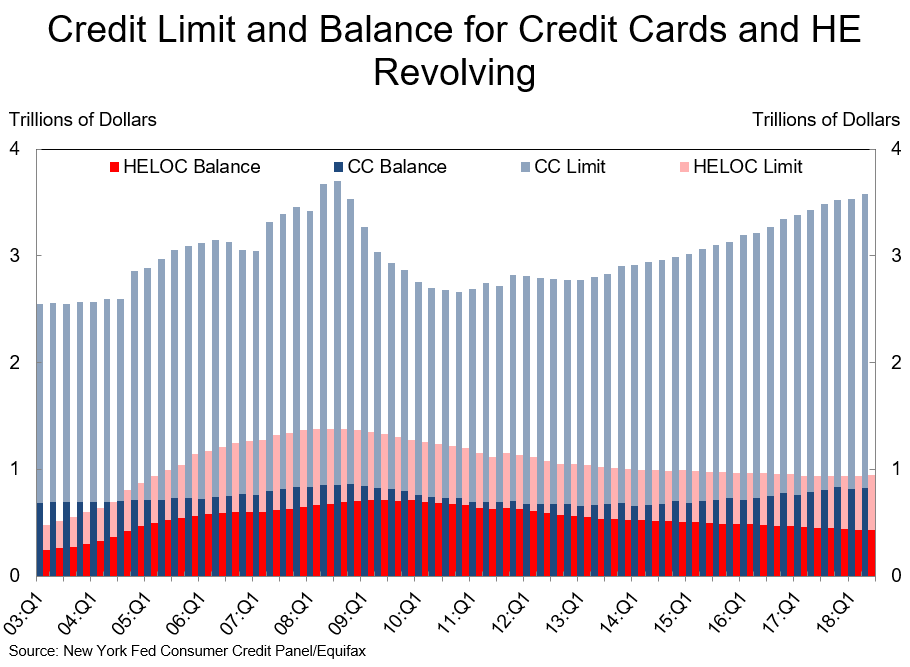

Credit card holders typically carry a relatively small balance relative to their spending limit. In recent years HELOC borrowers tended to use about half their loan limit on average.

While the terms and specifics of a HELOC can vary greatly from provider to provider, there are some commonalities shared by them all:

1

The lender will offer a set LTV, or loan-to-value limit on the amount you can borrow. They extend a line of credit to you for this amount.

2

There will be a draw period, usually 10 years (but it varies), during which you can spend up to your limit.

3

You will typically make interest-only payments during the draw period, at a variable interest rate set to an index, or benchmark rate…though this can vary by lender and offer. Most lenders also offer interest + principal payments, which can be beneficial to the borrower. More repayment options are detailed below.

4

Following the draw period is a longer repayment period where you pay back what you spent, plus interest. The interest rate is typically fixed during this period, but it also varies.

While these basics tend to hold true for most HELOCs, there are always exceptions and various offers to consider. By knowing more about the individual aspects of a HELOC, you can be more aware of who is extending your best possible offers.

The lenders who offer HELOCs will extend a percentage of your home’s value as your credit limit. They determine this amount by dividing the appraised value of the house by the amount remaining on your mortgage, and the amount you’d like extended.

For example, if your home is worth $300,000 and you owe $90,000 on it, divide the balance by the appraised value: 90,000/300,000= .3, or a 30% LTV ratio.

With a HELOC, your lender will look at a combined-loan-to-value ratio (CLTV), where they add the amount you want to borrow with how much you owe.

Using the example, if you wanted a credit line of $40,000, you’d add it to your loan balance, and divide by the appraised value: (40,000+90,000)/300,000=.43, so a 43% CLTV.

Lenders will offer different rates to qualified borrowers, but most lenders do not go above 80% CLTV, and some will stay lower, depending on the applicant’s qualifications. In some government programs, like VA, FHA and USDA loans, the LTV rate may be as much as 100%, so it is smart to research these options as they might apply to your specifics.

The following map can be used to explore offers from local lenders.

The draw period will range in time based on the lender and offer, but typical draw periods are set at ten years. During the draw period you do not have to spend all the credit you are extended, and you only pay (usually) on the money you spend.

Draw periods may range from 5 years to 20, but the average tends to fall in the middle. The payments you make during the draw period can revolve and restore your credit. So, if your line is for $40,000 and you use $20,000 and pay back $15,000, you’d then have $35,000 left to draw from.

Note that if you choose a draw period with principal + interest payments, your payments are likely to remain steady. Payments typically increase (when the draw period ends) when your draw period payments are interest-only. You can usually also pay extra principal if you have interest-only payments.

It is important to understand how long your draw period will be and what terms will apply to it. If you need money in a shorter time-frame for a known cost, maybe a HELOC is more than you need, and a home equity loan might be a smarter move for a lower overall cost.

If you are looking at needing smaller amounts spread out over time, the HELOC and its draw period can help you to save money by only using what you need, as needed. Making interest-only payments during this time can also free-up cash flow crucial to some situations.

Inactive Account Fees

Word of Warning: some lenders may leverage fees for inactivity during a draw period. Look at all of the fine print for your HELOC and understand the restrictions and expectations on usage.

Following the draw period, you will begin to repay the loan plus interest in a set repayment period, usually 10 to 20 years. This is a little shorter than a standard first mortgage, which is 30 years.

Repayment periods are usually governed by a fixed rate, though variable rates can be used as well. Typically, the draw period is variable and then the repayment period moves to a fixed rate, set as a percentage over the prime rate. Check with your lender and the specific terms of your deal to be sure of how it’s handled.

Payments made during the repayment period are amortized, meaning you make monthly payments of interest and principal. Over time, you will pay down the interest and pay more principal but expect steady payments for the duration of the repayment period.

Lenders will be seeking some standard things when qualifying an applicant for a HELOC. They are looking to minimize their risk, so it helps to understand how you can help improve your own chances of success.

Lenders will offer a HELOC at an APR that is using a margin over the prime rate. The margin is usually constant, but the prime rate may change a lot over the life of the loan. If a lender offers a HELOC under prime, chances are that the rate is short term.

Pay attention to the way the lender words their offer – it is common for a HELOC to have an “introductory rate” that is significantly discounted for a short period of time, like six months. This rate is a teaser, and the actual rate may be one that is higher than you’d like.

Ask specifically, what the margin will be for your HELOC. This is an important number to know for understanding what it will likely cost you over time, as well as helping you to compare offers.

There will be some associated closing costs with a HELOC, but they tend to be less than with a traditional mortgage. Lenders seldom charge points for a HELOC, but you will have some lender fees to consider.

Ask the lender if there is a minimum balance required, or a minimum draw at closing. Normally, the lender requires a draw at closing to ensure they are not offering a line of credit to someone who won’t use it. Some will require a monthly balance to avoid charging a maintenance fee.

You will typically pay a small annual fee, that is often waived for the first year or two. There may be a fee leveraged for cancellation or a lack of use, so make sure you know all the specifics.

As of 2017, the tax benefits from a HELOC require you to spend the proceeds on home remodeling and property updates. Deducting the interest paid on a HELOC would require that you spend it on updating your property. Keeping receipts on such projects is important to show how you used the funds.

For more information about the tax implications of your potential decision, visit the IRS.

The most popular uses for a HELOC, tend to be purchases like home repairs, annual education costs, a large expense, and debt consolidation.

| Type of Use | Home Equity Loan | Home Equity Line |

|---|---|---|

| Debt Consolidation | 44% | 40% |

| Home Improvement | 25% | 23% |

| Automobiles | 7% | 7% |

| Education | 4% | 6% |

| Major Purchases | 2% | 6% |

| Investment | 2% | 3% |

| Household Expenses | 2% | 2% |

| Business Expenses | 1% | 2% |

| Medical Bills | 1% | 1% |

| Vacation | 1% | 1% |

| Other | 11% | 9% |

For the annual costs, like a yearly tuition, a HELOC can be a smart move, offering you enough credit to cover the bill every year, and then time to pay some (or all) of it back to restore your credit line. Likewise, for the home repairs – these can be bills that are spread out over time, but need immediate attention to keep your projects rolling, so a HELOC can make a smart move to get it done.

Though a lot of consumers may look to a HELOC as a way to consolidate debt, it may be wise to look more specifically at how it compares in cost and risk to a home equity loan or a cash-out refinance.

Explore conventional mortgages, FHA loans, USDA loans, and VA loans to find out which option is right for you.

Check your options with a trusted El Monte lender.

Answer a few questions below and connect with a lender who can help you save today!