In recent years, a lot of focus has shifted to clean energy and programs that assist in the goal of creating and maintaining clean energy. There are many government programs that were designed specifically to help both residential and commercial buildings upgrade to clean energy options like solar panels and more efficient heating and cooling systems.

In early 2010, the Property Assessed Clean Energy (PACE) program was introduced. Any home or property owner who qualifies for this financing program gets funding to perform upgrades for clean energy options to their properties. They pay this funding back through property taxes. This article will go over the PACE program including a history, what projects are covered, how it works, advantages, disadvantages, and more. The goal is to give you a decent understanding of this program, as well as resources to find out more.

The PACE program is a government-funded financing program for individuals to upgrade their homes or businesses with clean energy alternatives. It is designed to finance 100% of the project cost upfront in the form of a lien on the property. The homeowner or business owner takes the funding they got from the program and performs upgrades like installing solar panels, upgrading the lighting to more energy efficient options, and installing more efficient heating and cooling systems on the property.

The PACE funding comes from either local government agency or a third-party financial entity. This program is like a traditional loan in the fact that there is a set repayment term typically from five to twenty years, and it has an interest rate that is added to the loan. However, it differs from a traditional loan because the PACE funding becomes tied to the property itself in the form of the lien and not to the property owners.

This program was debuted to the general public in 2005, but the structure and general idea for this type of program had been around since early 2001 with solar bonds. The San Francisco area voters wanted a program to fight the high upfront costs that came with upgrading your home or business to more energy efficient options like solar panels. It isn't hard for a homeowner to spend over $20,000 to install a solar panel system on their homes, but they typically won't get all of the cost back if they decide to sell the property. The PACE program allows homeowners to take out a mortgage-type of a loan on the property, and they'll only pay it for as long as they live there. Should they move, the new property owner will be responsible for continuing to pay the fees until it's paid off or they move.

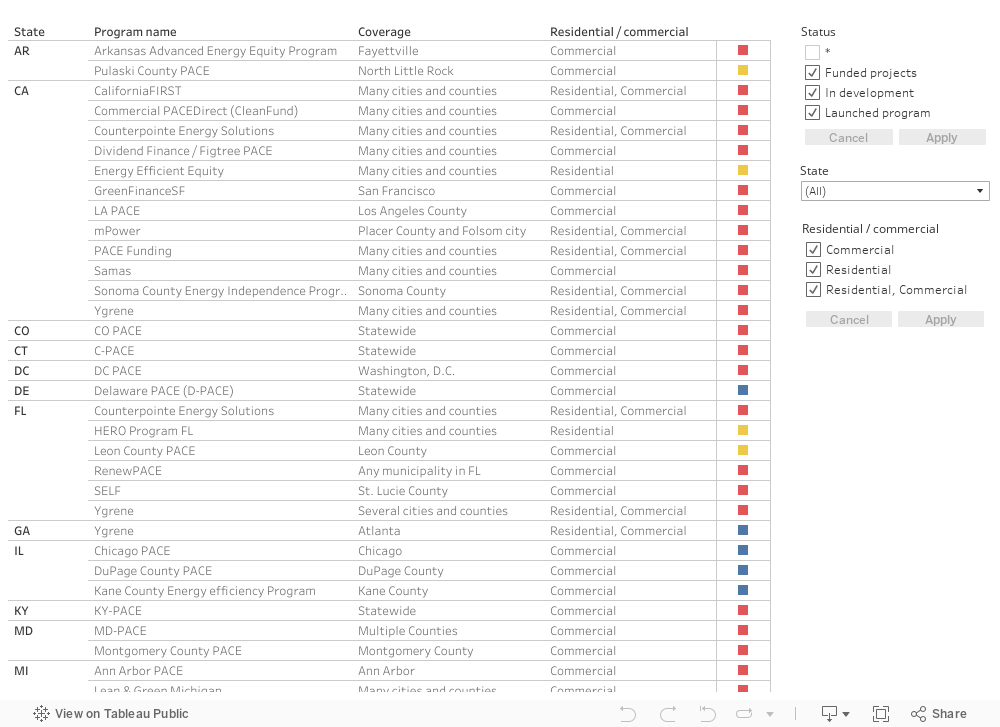

PACE began in Berkeley, California at the University of California, Berkeley. PACE was developed using the Guide to Energy Efficiency & Renewable Energy Financing Districts for Local Governments. This guide got its funding from grants from the United States Environmental Protection Agency and the city of Berkeley. It was thought that this program would be a way to lower the pollution rate of the San Francisco Bay and help them reach their climate goals. In 2008, the BerkeleyFIRST Climate Program was launched and legislators voted to move forward with financing the PACE program under this name. To date, 34 states passed legislation to allow PACE program funding.

The PACE program can cover a variety of projects on both residential and commercial buildings. It will cover the cost 100% upfront, and the homeowner will repay it over a set term with interest. We will go over a few of the more popular upgrades that homeowners choose to use their PACE funding for.

If you own your property and you want to make it more energy efficient, you should check to see if you state supports PACE financing. To date, 34 states have some kind of PACE financing program in place for residents to use.

Once you've checked to see if you state supports the PACE program, you want to contact a PACE lender directly. If you get your information from a second party, they may forget important information like how much you'll have to pay, or if there are any specific requirements, you'll have to meet.

You'll need several documents for proof to successfully complete the application process. This entire process requires a lot of work on the homeowners part before they even get to the PACE lender's office. These documents may vary from state to state, but generally, they will need:

As soon as you've spoken to a PACE lender and you've decided that you want to pursue PACE funding, you can begin the application process. This process will vary from state to state, and you have to start on a state level to get off to the right start. Your PACE lender can point you in the right direction.

You can fill out the application in-person at the PACE lender's office or online with a downloadable PDF form. When you've completed the application, you can mail, email, fax, or deliver in person to the PACE office. You should get notification within 24 hours if your application has been accepted.

The application should be accepted as soon as the state PACE office gets it. If you don't hear anything within 24 hours, contact them. Once your application is accepted, it'll be processed and either approved or denied. If your application is accepted, the funds will be released, and you can use them for your project.

You'll begin repayment on your PACE loan once your property taxes are due again. You'll pay a set amount once a year until you vacate the property or you pay off your PACE funding. It'll show up on your annual property tax bill as a separate charge, and you pay it when you pay your annual taxes.

The PACE program is split into two separate programs, commercial and residential. Each program is built on the same foundation, and they have the same goals to reduce energy use and be more environmentally friendly.

Residential PACE or (R-PACE) is currently operational in 34 states and it also offers 100% upfront financing for residential buildings.

This program covers 100% of the labor fees and installation costs of energy-efficient upgrades. If the household is lower income, or if they can't allocate the funds to make their homes more energy-efficient, the PACE program can help. A few other benefits of the residential PACE portion of the program include:

Commercial PACE (C-PACE) is currently operational in 16 states and it offers 100% upfront financing for commercial, industrial buildings, multifamily housing, and nonprofit properties. If the business owner opened a new business or if they're running a non-profit, this is critical as they tend to have limited budgets to being with. This program gives business owners a chance to secure long-term, low-cost financing to perform upgrades to their buildings. Currently, the payback term has been extended for up to 20 years. Other benefits include:

Since it was introduced, the PACE program has offered many benefits for both residential and commercial property owners. Aside from the obvious savings, there may be a few you don't realize.

This program is easier to qualify for than most loan-type programs. PACE doesn't focus heavily on your credit score or your credit history. It concentrates on the home's equity, property tax status, and any payment history. This can help people who don't have the best credit or have a thin credit history.

The extended repayment plan can stretch up to 20 years. This has the potential to lower the yearly payments, and take some of the stress away with trying to come up with the money to cover them. You should keep in mind that the longer you draw out your repayment plan, the more interest that'll be added onto the balance.

The PACE program will cover every cost for the project from start to finish. This 100% coverage will allow lower income households and non-profits or new business owners to afford to make their home more energy-efficient. It covers everything from labor costs, miscellaneous fees, and any equipment costs.

Once the PACE project installation process begins, you may become eligible for tax deductions or credits. However, it is a good idea to check with your tax accountant on the specific credits or deductions. Many of them may only make it possible to get credit for the year they're installed, and if it's not claimed within that year, you miss out. Be aware that some of the scammier players in the market do not pass the tax deductions onto the homeowner. The big problem with tax breaks is most people do not make enough income for them to make a difference when compared against taking an ordinary standard deduction.

Chavez said the company that pitched her on the panels, Fidelity Home Energy, did not explain how expensive they would be, nor suggest that she consider a different means of financing other than the loan they offered, which has a 10.32% interest rate and gets paid as part of her mortgage bill. They did tell her she’d get a $10,000 tax break – but not that such an incentive is useless to people at her income level.

The 2018 tax bill allows mortgage interest deduction on interest payments for up to $750,000 of mortgage debt, but no longer allows the deduction of interest paid on HELOCs or home equity loans unless the debt is obtained to build or substantially improve the homeowner's dwelling.

The PACE program attaches to the property itself and not the property owner. This means that if you sell the house or business, or if you rent it out, the new tenant will be responsible for the payment. So you won't have to repay more than you put in, and this will work to save you money.

Even though there are several benefits, there are steep pitfalls to this program as well. Before you commit yourself to the PACE program, you should do your research and learn what you could lose.

Unfortunately, if a home or business owner hears about the PACE program from a contractor, the contractor could be biased or have ulterior motives. The contractor stands to get a decent amount of funding for the project and a referral fee. Many contractors get a $500 kickback for a referral. This could make them push the PACE program while not talking about the potential drawbacks. They could also inflate their prices in an attempt to get more money for their work, as many homeowners are unaware of the full cost of something that is spread out over time. The Wall Street Journal published an article comparing the fast-growing PACE program to subprime loans during the housing bubble. That article states

The largest PACE lender, Renovate America Inc., is accused in three lawsuits filed in November by borrowers of double-charging interest and administrative fees and failing to immediately credit loan payments. The suits seek class-action status.

The FBI and SEC are investigating Renovate America's business practices:

FBI agents are seeking documents that show how Renovate America marketed its financing to homeowners, trained its sales force and outside contractors, and communicated with investors, according to a document reviewed by the Journal. The FBI also is conducting interviews of people familiar with the company, according to the people who have been interviewed.

…

The Journal has reported that Renovate America has made payments for some borrowers who have struggled to pay their loans without telling Wall Street investors who buy bonds packaged with the company’s loans. Securities laws require companies to disclose all information that investors would consider to be material.

Pricing irregularities are widespread in the industry. Elon Musk's SolarCity paid $29.5 million to settle allegations they submitted inflated claims to the U.S. Department of Treasury.

PACE loans are actually mortgages, only they have lacked the standard disclosures required on traditional mortgages.

“Predatory green-energy lenders are changing state and local laws to trick seniors into taking out high-interest rate loans for 20 years, along with liens on their homes, for technology that could be obsolete in a few years,” Cotton continued.

“Today, these loans are exempt from the same disclosure forms required for other home loans,” Cotton added. “Our bill will fix this. Requiring disclosure will reduce the advantage that PACE loan sharks have over hard-working Americans. It's just the accountability we need.”

One of the biggest risks of the PACE program is the risk for foreclosure. The contract for the funding will act as a lien on the property. If you fall behind on your payments, you risk losing their home or business to foreclosure. Even if you're current on your mortgage payments, the PACE program moves in front of it, and they can start foreclosure proceedings.

Everett Cain, 87, says he and his wife are on the verge of foreclosure after a contractor representing Renovate America said a PACE loan would “be a complete financial wash” and wouldn’t cost anything. Instead, his annual tax bill jumped from $800 to roughly $4,000.

…

The PACE program, Mr. Cain said, “is a great way to steal someone’s home.”

This program is designed for people who can't afford other loans due to credit issues or income limits. If you add new windows to your home, it has the potential to increase the home's value. However, many PACE programs do not back out economically - which is part of the reason there are governmental subsidies - to offset the poor economics.

The PACE fees are paid once a year, or twice at the most, typically as an assessment added to the property-tax bill. This can result in an inflated payment that a home or business owner may not be ready to pay. It may be a possibility to have the PACE payments added onto the monthly mortgage payment to reduce any sticker shock, but this possibility is up to the lender.

A borrower will have to pay interest costs for any PACE funding. The more they extend their repayment plans, the more interest they'll end up paying over the life of their loan. This has the potential to add thousands of dollars to the initial payment amount, and they'll pay it for as long as they have a balance to repay. Some of these contracts last for decades. While solar technology improves driving down the cost of energy for people with new units on their roof, some homeowners will be stuck artificially high prices & interest for outdated technology.

The typical PACE loan averages about $25,000 but the range can fall anywhere between $5,000 to $100,000. Here is a table which shows examples of the math behind the loans.

| Low | Average | High | |

|---|---|---|---|

| PACE Loan Amount | $5,000 | $25,000 | $100,000 |

| APR | 6% | 7.5% | 9% |

| Repayment Period | 5 years | 15 years | 25 years |

| Interest Cost | $799.89 | $16,716.05 | $151,755.92 |

| Total Cost | $5,799.89 | $41,716.05 | $251,755.92 |

| Inteest Cost as % of Total | 13.79% | 40.07% | 60.28% |

| Annual Loan Payments | $1,159.98 | $2,781.07 | $10,070.24 |

For a PACE program to make economic sense the energy cost savings need to exceed the loan payments with interest.

If a payment is missed, PACE loans can accrue interest at 18% annually.

What's more, the above loans are at significantly higher rates than mortgages. As of the date of publication of this article, here is a list of prevailing rates nationwide.

| Loan | Rate | Type | Years |

|---|---|---|---|

| 30-yr | 4.04% | fixed | 30 |

| 15-year | 3.25% | fixed | 15 |

| 5/1 ARM | 3.52% | variable | 30 |

| Home Equtiy Line of Credit | 4.7% | variable | 10 |

| Home Equity Loan | 4.69% | fixed | 5 |

| Home Equity Loan | 5.14% | fixed | 10 |

| Home Equity Loan | 5.54% | fixed | 15 |

| Home Equity Loan | 6.09% | fixed | 20 |

| Home Equity Loan | 6.54% | fixed | 30 |

The following table lists current local mortgage rates.

As soon as you've gotten your PACE funding and you've gotten your project started, you'll want to start thinking about repaying it. Traditionally, your PACE payment will happen each year when you pay your property taxes. It is usually added on as a separate charge, and you simply pay it when you either send it or deliver your payment in-person. All of the yearly interest will be rolled into this payment as well. You may be able to have your PACE payment broken down into smaller portions that you'll pay each month. However, this is something you'll have to discuss with your PACE lender when you first talk with them about financing.

The amount of your payments and the length of your repayment plan depends on how much you're able to pay each year. You can set up a shorter repayment term, but your annual payments will be higher in cost. You can also opt to lower your monthly payments by extending your repayment term up to 20 years. Keep in mind that you'll pay out more in interest by extending your repayment plan.

If you decide to apply and secure funding from the PACE program, you want to avoid missing payments or defaulting on your repayment plan at all costs. The negative repercussions can be staggering. When you secure funding through the PACE program, there will be a lien put on the property. This will be put in front of your mortgage, so if you fall behind on your PACE payment but stay current on your mortgage, you could still face foreclosure.

Normally, once you've missed your first payment, foreclosure proceedings could begin in as little as three to six months. If you don't catch up very quickly, you can lose your home, and your credit will also take a large hit. Once you have a foreclosure on your credit history, it can take up to seven years before any lender will feel comfortable enough to extend you a line of credit to purchase another home.

The PACE program was originally called the HERO program. Before you get this lien on your property, you should be aware of potential property value impacts. This will be extremely important if you plan to sell the home before you've completely paid off your PACE loan.

You have to know that it the PACE program acts as a lien on the property and that it is considered the priority lien. Meaning that the PACE loan's balance will get paid off first before the mortgage if the homeowner defaults. This is extremely important because mortgage companies Frannie Mae and Freddie don't want their loan's position threatened by the PACE program, and they control around 90% of the mortgages in the United States.

This means that any homeowner who wants to refinance their existing mortgages with Frannie Mae or Freddie Mac financing will be blocked from doing so until their PACE loan is paid off. Any buyer who wants to purchase a property with a Frannie Mae or Freddie Mac mortgage won't be allowed to as long as there is a PACE lien attached to the property. This has the potential to have a negative impact on the property value. It has a very good chance of not selling until the PACE lien is removed.

Additionally, if you don't call your mortgage company as soon as you get funding from the PACE program, you'll end up with a deficit. This will show up in your impound or escrow account for your property taxes. If you have a deficiency in your escrow account, your financial lender may require you to pay it within 30 days. Many people don't have this money available, and it can lead to more financial trouble.

You should do your research and shop around before you commit to any loan for your property. There are alternative programs to the PACE program that may work out better for your situation. You don't want to lock yourself into a loan program and realize you're in over your head. DSIRE maintains a comprehensive nationwide database of clean & renewable energy policies and incentives across the nation. Homeowners who do not want the ongoing overhead of a PACE loan may qualify for other local incentive programs. For many homeowners a home equity loan or a line of credit might be more appropriate.

| Feature | Home Equity Loan | HELOC | Cash Out Refi |

|---|---|---|---|

| Fixed Interest | Yes | No | Yes |

| Adjustable Interest | No | Yes | No |

| Lump Sum Payment | Yes | No | Yes |

| Borrow As You Need It | No | Yes | No |

| Interest-Only Payments | No | Yes | No |

| Interest is Tax Deductible | Yes * | Yes * | Yes * |

* Provided the debt is obtained to build or substantially improve the homeowner's dwelling.

The Federal Reserve has hinted they are likely to taper their bond buying program later this year. Lock in today's low rates and save on your loan.

Are you paying too much for your mortgage?

Check your refinance options with a trusted El Monte lender.

Answer a few questions below and connect with a lender who can help you refinance and save today!